Introduction

Real estate is critical to most economies, particularly in land-scarce regions such as Hong Kong and Singapore. It plays a significant role in the functioning of their respective economies (Haila, 2000). Over the past few decades, as major financial hubs in Asia, Hong Kong and Singapore have witnessed notable transformations in their real estate markets. In addition to rising property prices, policy framework adjustments have been made. Despite similarities in geographical locations and market environments, the policy trajectories of the two regions have diverged, particularly concerning stamp duty on real estate transactions.

On February 28, 2024, Hong Kong officially abolished the Buyer’s Stamp Duty (BSD) on residential properties through the Public Revenue Protection (Stamp Duty) Order 2024. Conversely, in 2023, Singapore enhanced the Buyer’s Stamp Duty and the Additional Buyer’s Stamp Duty on high-value residential properties. This leads to the research question: How will the abolishment of stamp duty by Hong Kong and the increase in stamp duty on high-value residential property by Singapore affect their respective real estate markets in comparable market conditions?

Using the Most Similar Systems Design (MSSD) and the Theory of Change (TOC) as research frameworks helps establish necessary and sufficient conditions for an explanation based on qualitative research. MSSD assists in analysing the effects of policy differences under the same contexts and facilitates an exact assessment of the impacts of different policies on real estate markets operating between the two regions. TOC helps investigate the short-run and long-run impacts of these policies on market activity, prices of property, and liquidity, as well as the factors and causal mechanisms responsible for these changes.

This study, therefore, compares the difference in stamp duty policy between Hong Kong and Singapore, analyses its impact on the real estate market, and provides valuable lessons for policymakers in other regions to inform the formulation of real estate policies.

Literature review

Stamp duty on real estate refers to a type of property transaction tax levied concerning the transfer of property ownership. Usually, stamp duty is computed as the percentage of the purchase price the property is subjected to, and it is usually paid at the time of the transaction by the buyer (Cho et al., 2021). The logic behind stamp duty is to cool off overheated real estate markets through reduced speculative purchases, hence stabilisation of property prices. It generates government revenue and helps to regulate the real estate market by increasing transaction costs, which may reduce demand and soften rapid price increases (Wong et al., 2021).

Real estate policy refers to the regulations and guidelines formulated by the government to manage and influence the real estate market (Shao et al., 2020). These stamp duty policies were meant to suppress speculative activities, which drive up the prices of properties in Hong Kong. Taxation of property transactions has, therefore, been one of the ways to stabilise the market and ensure that property prices do not proliferate (Craig & Hua, 2011). According to Chui et al. (2019), Hong Kong’s stamp duty is part of a set of “cooling measures” that raise transaction costs for buyers. However, these measures have not been able to bring down the prices because of the strong market demand. Hui et al. (2017) note that Hong Kong’s Special Stamp Duty significantly cuts transaction volumes, with a long-term effect on more significant properties and less pronounced for smaller properties. Ho et al. (2022) argue that the SSD has led to a decline in overall market turnover, thus sharply reducing the supply of secondary-market housing, which drives up prices in this segment.

In Singapore, stamp duty policies aim to regulate real estate transactions and generate government revenue by managing housing market demand, particularly from foreign buyers. This helps to stabilise property prices and ensure housing affordability for residents (Phang et al., 2014). Zhang et al. (2023) noted that Seller’s Stamp Duty in Singapore reduces market liquidity and depresses the probability of sale for properties by increasing the opportunity costs for locked-in sellers to sell at higher prices compared with non-locked-in sellers, thus significantly impacting the private housing market. Chen et al. (2023) argued that Singapore’s new stamp duty regime has fueled property price increases and affected market dynamics.

MSSD is a research strategy in comparative political studies where systems are selected to be as similar as possible, except for variation in one particular phenomenon, the independent variable. The goal is to study the effect of the independent variable on the dependent variable while screening out as many external variables as possible. This approach enables researchers to minimise other system differences and focus exclusively on a single variable (Anckar, 2008). To mitigate speculative activities in the real estate market, several Asian cities have implemented tiered transaction taxes based on the holding period of properties. Hong Kong and Singapore introduced such time-dependent transaction taxes in 2010 (Tam, 2018). According to Phang (2000), Hong Kong and Singapore share numerous similarities in geography, economy, history, international positioning, population, land resources, and real estate markets. Therefore, Hong Kong and Singapore are comparable. Using the MSSD approach to compare the differences in real estate policies between Hong Kong and Singapore allows for a better analysis of the direct impacts of policies on the real estate market while controlling for their economic and geographic similarities.

The TOC is a project-specific, logical framework that outlines the rationale for a project, describes the steps for implementation, and details the underlying assumptions to ensure more focused and systematic execution (Reinholz & Andrews, 2020). In the context of policy evaluations, Maye et al. (2020) argue that the TOC framework should be used to go beyond just determining whether a policy works by establishing how it works, under what circumstances, and for whom. Therefore, TOC can be used to validate the effectiveness of real estate policies in Hong Kong and Singapore and systematically assess their short- and long-term impacts on the market.

Policy Overview

In 2022, the median price of private residential properties in Hong Kong was USD 1.16 million, making it the second most expensive city for housing prices in the Asia-Pacific region, surpassed only by Singapore. However, compared to 2021, housing prices in Hong Kong fell by 8.7%. The median rent in Hong Kong was USD 1,686, second only to Singapore (ULI Asia Pacific, 2023). Despite the decline in housing prices and rents, they remain high, and the affordability issue for ordinary residents has not been fundamentally addressed.

On February 28, 2024, the Hong Kong Special Administrative Region Government announced the Public Revenue Protection (Stamp Duty) Order 2024, which immediately abolished all demand management measures on residential properties. This meant that additional stamp duty, buyer’s stamp duty, and new residential stamp duty were no longer required for residential property transactions. The document highlighted the market context behind this adjustment: since the relaxation of residential property demand management measures on October 25, 2023, the residential market has not shown signs of overheating. While transaction volumes had increased slightly, they remained below levels seen in the first half of the year, housing prices continued to decline, demand was sluggish, speculative activities and foreign investment demand remained low, and housing supply was sufficient. It was projected that the market would remain stable in the coming years.

This policy can also be seen as an extension of the adjustments made in 2023. In announcing the 2024–2025 fiscal year budget on February 28, 2024, Hong Kong’s Financial Secretary, Paul Chan Mo-po, reiterated that the adjustments to residential property demand management measures introduced on October 25, 2023, included shortening the applicable period for additional stamp duty from three years to two years, halving the rates for buyer’s stamp duty and new residential stamp duty, and implementing a “pay first, refund later” arrangement for foreign talent purchasing properties. This arrangement was well-received, demonstrating Hong Kong’s appeal to foreign talent. These adjustments aimed to achieve critical objectives of the government’s housing policy: revitalising the real estate market, restoring buyer confidence, attracting overseas investors, increasing market liquidity, and maintaining the robust development of the private residential property market (Hong Kong Special Administrative Region Government, 2024, February 28).

According to ULI Asia Pacific (2023), the median price of private-sector homes in Singapore reached USD 1.2 million in 2022, making it the most expensive city in the Asia-Pacific region. The median monthly rent for private housing was USD 2,596, significantly higher than Hong Kong’s USD 1,686. These figures indicate that Singapore’s real estate market continues to heat up. As the region’s most expensive city, the rising property prices and rents in Singapore have become a critical issue for the government.

On February 14, 2023, the Singaporean government announced in its fiscal budget that the buyer’s stamp duty rate for high-value residential properties would be increased to a maximum of 6%, affecting transactions for properties worth over SGD 1.5 million. Later, on April 26, 2023, the government further increased the Additional Buyer’s Stamp Duty (ABSD) rates, mainly targeting foreign buyers (from 30% to 60%) and local purchasers of multiple properties. These policies aimed to curb speculative demand, with the private residential market being their primary focus. In contrast, the public housing market remained relatively stable, as prices in this segment are strictly regulated and managed by the Housing and Development Board (HDB). Public housing primarily meets the self-occupancy needs of citizens, and transaction prices typically fall below the range affected by buyer’s stamp duty adjustments. The HDB resale market is also not subject to ABSD. The government aims to suppress demand in the high-end residential market and speculative purchases by foreign buyers and local investors while ensuring affordable housing for local families and maintaining overall real estate market stability.

Such a hike in stamp duties by the Singaporean government for high-value homebuyers is part of a measured approach to tempering excessive foreign demand, thereby stabilising prices of property that will help address the population growth-housing supply imbalance (Phang et al., 2014). In general, Singapore levies high stamp duties for high-value properties. According to Haila (2022), such a strategy is supposed to put a brake on the real estate market and moderate its negative impact on the labour market due to the increase in the cost of housing. The mechanism allows Singapore to reap increased tax revenues from foreign buyers and the wealthy, which can be used to finance public resources and keep the market in equilibrium at an affordable level.

While the real estate markets of Hong Kong and Singapore have some similarities, their respective buyer’s stamp duty policies vary significantly in 2023–2024. Hong Kong has abolished buyer’s stamp duties to rejuvenate the market and lure foreign talent. In contrast, Singapore is hiking the rates, especially for foreign buyers and high-value homes, to contain speculative demand and keep the market steady. Measures in Hong Kong are targeted at the short-term recovery of market vitality, while in Singapore, high buyer’s stamp duties are tools that policies use to regulate the real estate market and transform tax revenue into public resources to balance supply and demand for housing affordability.

Policy Impact Analysis: A Comparison Based on MSSD

This study employs the MSSD to analyse the differing impacts of Hong Kong’s abolition of BSD and Singapore’s increase in BSD and ABSD on their respective real estate markets. Given the high degree of similarity between the two regions regarding economic and geographical contexts, MSSD effectively isolates similar external variables to highlight the effects of differing policies.

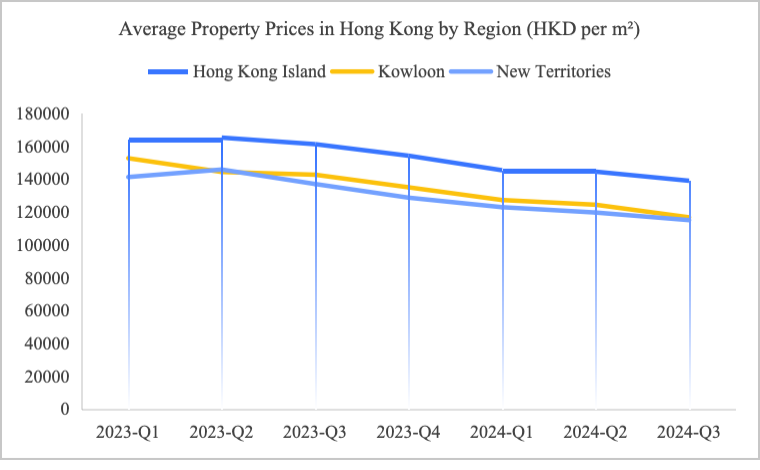

Hong Kong’s Open Data platform provides property market statistics compiled by the Hong Kong Land Registry, which includes data on property prices and transaction volumes from Q1 2023 to Q3 2024. Figure 1 illustrates the average property prices in Hong Kong Island, Kowloon, and the New Territories. The original data includes less than 40 square meters, 40 to 69.9 square meters, 70 to 99.9 square meters, 100 to 159.9 square meters, and 160 square meters or more. For simplicity, the averages of these categories were calculated. Figure 2 records the transaction volumes of second-hand properties during this period (DATA.GOV.HK, 2024).

Figure 1 shows a continued decline in overall average property prices in Hong Kong. Figure 2 shows that the transaction volume of second-hand properties peaked at 11,218 in Q1 2023 but then fell steadily, reaching a low of 5,744 in Q4 2023. However, transaction volumes rebounded significantly after Q1 2024, peaking at 11,403 in Q2 2024 before slightly declining to 7,724 in Q3 2024.

This trend reflects a lagged market response to the policy changes. Second-hand property transactions did not increase rapidly in the short term; they declined continuously from Q2 to Q4 2023. Only after Q1 2024 did transaction volumes recover, indicating that the market gradually absorbed the policy’s effects. The sustained decline in property prices and transaction volumes during the early stages of the policy implementation suggests that the policy failed to boost market confidence in the short term. However, the significant rebound in transaction volumes starting in 2024 indicates that the policy gradually achieved its intended effect of revitalising the housing market, which aligns with the Hong Kong SAR Government’s expectations.

Despite this recovery in transaction volumes, property prices did not increase in tandem, highlighting the persistent structural challenges Hong Kong’s real estate market faced. This suggests that further policy interventions may be necessary to stimulate a full market recovery.

Figure 1

Average Property Prices in Hong Kong by Region (2023-Q1 to 2024-Q3, HKD per m²)

Figure 2

Secondary Property Transactions in Hong Kong (2023-Q1 to 2024-Q3)

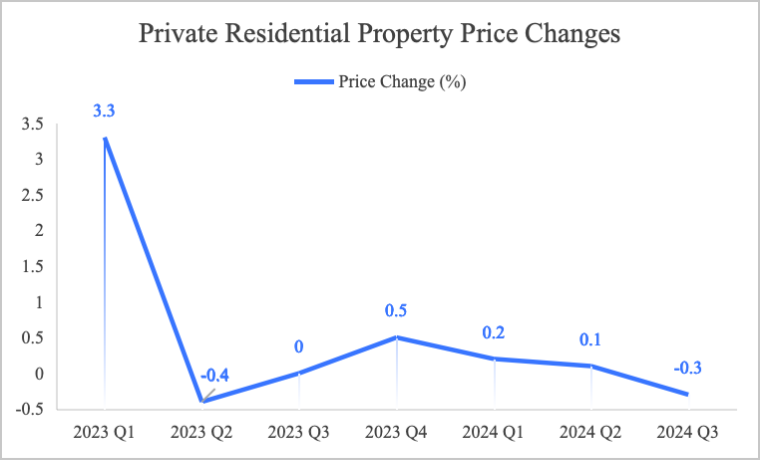

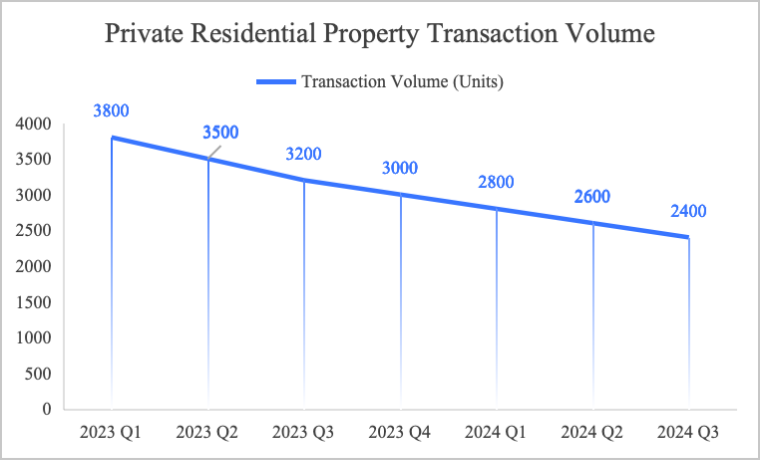

Singapore’s Urban Redevelopment Authority (URA) website provides data on property prices and transaction volumes from Q1 2023 to Q3 2024. Figure 3 illustrates the price trends in Singapore’s private residential market from Q1 2023 to Q2 2024, while Figure 4 shows transaction volume changes in the same market from Q1 2023 to Q3 2024 (URA, 2023a–2024c). These data reflect the significant impact of the Singapore government’s increase in BSD and ABSD policies.

Following the government’s announcement of increased BSD in Q1 2023, there was a surge in pre-policy implementation purchases, resulting in a 3.3% price increase and maintaining transaction volumes at a high of 3,800 units. However, with the policy taking effect on February 14, 2023, and the government further increasing ABSD rates on April 26, 2023—raising taxes for foreign buyers by 60% and for local multiple-property buyers by 20%–30%—speculative demand was further suppressed. This led to a 0.4% price decline and a drop in transaction volumes to 3,500 units in Q2 2023.

From Q3 2023, the market began stabilising, with transaction volumes falling to 3,200 units, indicating a sharp reduction in speculative demand. Private residential prices saw a brief 0.5% recovery in Q4 2023. However, as 2024 progressed, the rate of price increases gradually narrowed, with a 0.3% decline recorded in Q3 2024. Transaction volumes indicated a long-term downward trend, reaching 2,400 units by Q3 2024.

These trends indeed reflect the long-term effects of Singapore’s policy measures. The restrictive tax rates have effectively curbed speculative demand for high-value properties and reduced purchasing activity among foreign buyers, eventually pushing the real estate market to the low-activity adjustment period.

Figure 3

Private Residential Property Price Changes (2023-Q1 to 2024-Q3)

Figure 4

Private Residential Property Transaction Volume (2023-Q1 to 2024-Q3)

In general, Hong Kong’s stimulus-oriented policy of abolishing the BSD had minimal short-run effects on property prices and transaction volumes. By contrast, Singapore’s demand-suppressing policies effectively curbed overheating in its market. Simply reducing transaction costs is insufficient to revitalise the real estate market fully. While removing BSD alleviated some burdens for investors, it failed to address fundamental issues such as the heavy financial pressure on homebuyers and a lack of market confidence. This policy would require complementary stimulus measures to rejuvenate Hong Kong’s property market significantly.

On the other hand, Singapore’s suppression-oriented measures prompted market adjustments in the short term but ultimately fostered more stable development in the real estate market. These cases demonstrate that demand-stimulating policies require accompanying economic incentives and confidence-building measures, while demand-suppressing policies must carefully weigh their long-term impacts on the market.

Policy Impact Analysis: Based on TOC

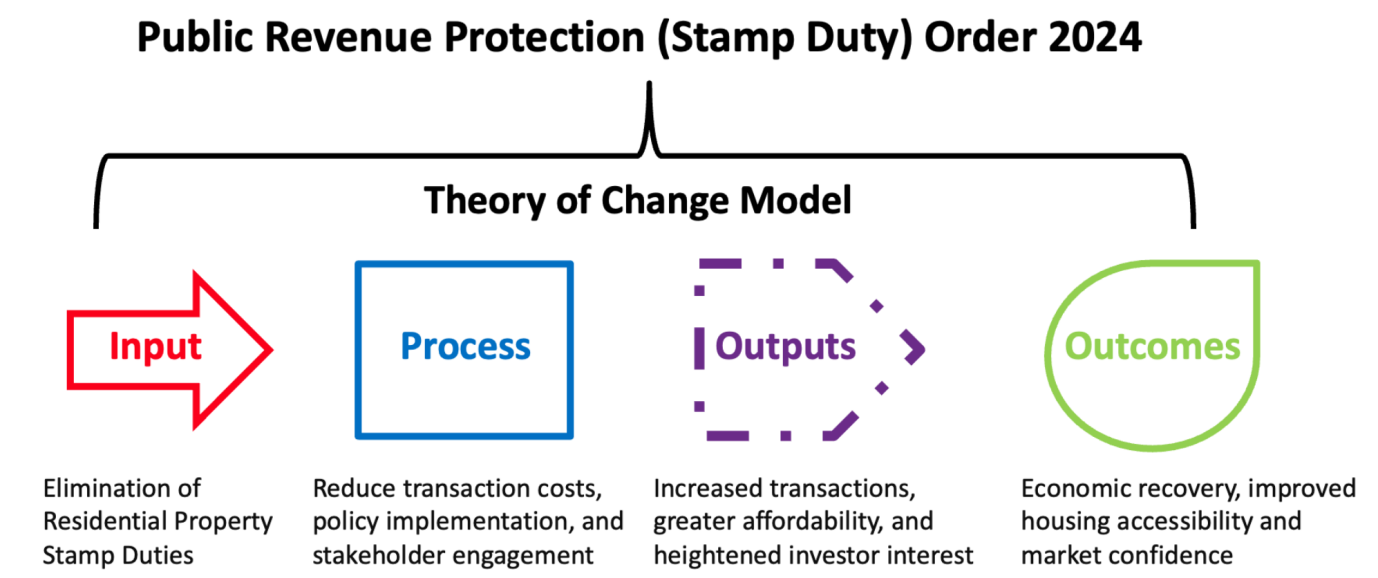

This study uses the TOC model in combination with the data presented earlier to analyse the stamp duty policies of Hong Kong and Singapore. The study posits that Hong Kong’s policy's short-term goal is to increase transaction volumes and reduce transaction costs; the medium-term goal is to restore public confidence in Hong Kong’s real estate market; and the long-term goal is to revitalise the property market and accelerate Hong Kong’s economic recovery. The policy's target audience includes non-local buyers, first-time homebuyers, and investors.

As shown in Figure 5, the analysis focuses on the policy’s inputs, processes, outputs, and outcomes.

In terms of inputs, to address the sluggish real estate market in Hong Kong, the Hong Kong SAR Government introduced a policy to abolish the Buyer’s Stamp Duty, aiming to attract buyers by reducing transaction costs and increasing transaction volumes. From a micro perspective, this policy benefits its target audience by lowering property transaction costs through the abolition of BSD, enhancing the willingness of buyers to participate in the real estate market, and attracting non-local buyers, such as high-end talent and first-time homebuyers, to purchase the property. It also increases investors' willingness to invest in property in Hong Kong’s real estate market. From a macro perspective, implementing this policy helps increase the derived revenues of the real estate market, boost real estate agents' incomes, drive demand for renovations and furniture, and promote the development of financial loan services.

Regarding the process, The government lowered the threshold for real estate transactions by abolishing the Buyer’s Stamp Duty, directly targeting the demand side of the market. The policy is designed to attract the return of non-local buyers and investors while reducing transaction costs for first-time homebuyers, thereby revitalising market activity. Various stakeholders are critical to the policy’s implementation. The government acts as the policy maker and promoter. With the lower thresholds for property transactions, the policy’s target audience becomes the primary beneficiary, whose participation and attention reflect the policy’s transmission effectiveness. Real estate agencies and related industries, such as renovations, help promote the policy and increase transaction volumes through advertising, further spreading the policy. The professional services they provide not only improve transaction efficiency but also stimulate demand in the real estate market. Financial institutions provide loan services, enhancing liquidity.

In terms of outputs, the policy is expected to result in four short-term direct outcomes. First, an increase in market activity is evident, as seen in Figure 2, where Hong Kong’s second-hand real estate transaction volumes showed a significant rebound starting in Q1 2024. Second, greater affordability is reflected, as shown in Figure 1, where property prices in Hong Kong remained weak, and the government’s abolition of BSD has reduced financial pressure on homebuyers and investors. Third, the policy has increased investor interest, with the rebound in transaction volumes indicating growing confidence in the real estate market, stimulating investment demand. Fourth, the abolition of BSD reduces government revenue.

In terms of outcomes, the policy is expected to lead to several medium- and long-term impacts. First, the policy can promote overall economic recovery by revitalising the real estate market, which drives the economic benefits of related industries, such as real estate agencies, furniture and renovations, and financial services, thereby enhancing capital liquidity. Second, Hong Kong’s real estate market will maintain long-term stability. The market will return to a healthy state, with transaction volumes increasing and prices stabilising. Third, the policy can restore investor confidence. As the real estate market revitalises and transaction costs decrease, investors are more willing to channel capital into Hong Kong’s real estate market. Fourth, Hong Kong’s global position will be enhanced. Compared to Singapore’s high-tax policies, Hong Kong’s tax advantages send a friendly signal to global investors. This advantage helps attract international capital and strengthens Hong Kong’s appeal as an international financial centre. Finally, the government’s fiscal revenue will also grow indirectly. With the rise in transaction volumes, related industries will also grow, and their growth will bring more tax revenue to the government. In the long term, the policy will positively impact government finances.

Figure 5

Using the TOC model to analyse Hong Kong’s Stamp Duty Policy 2024

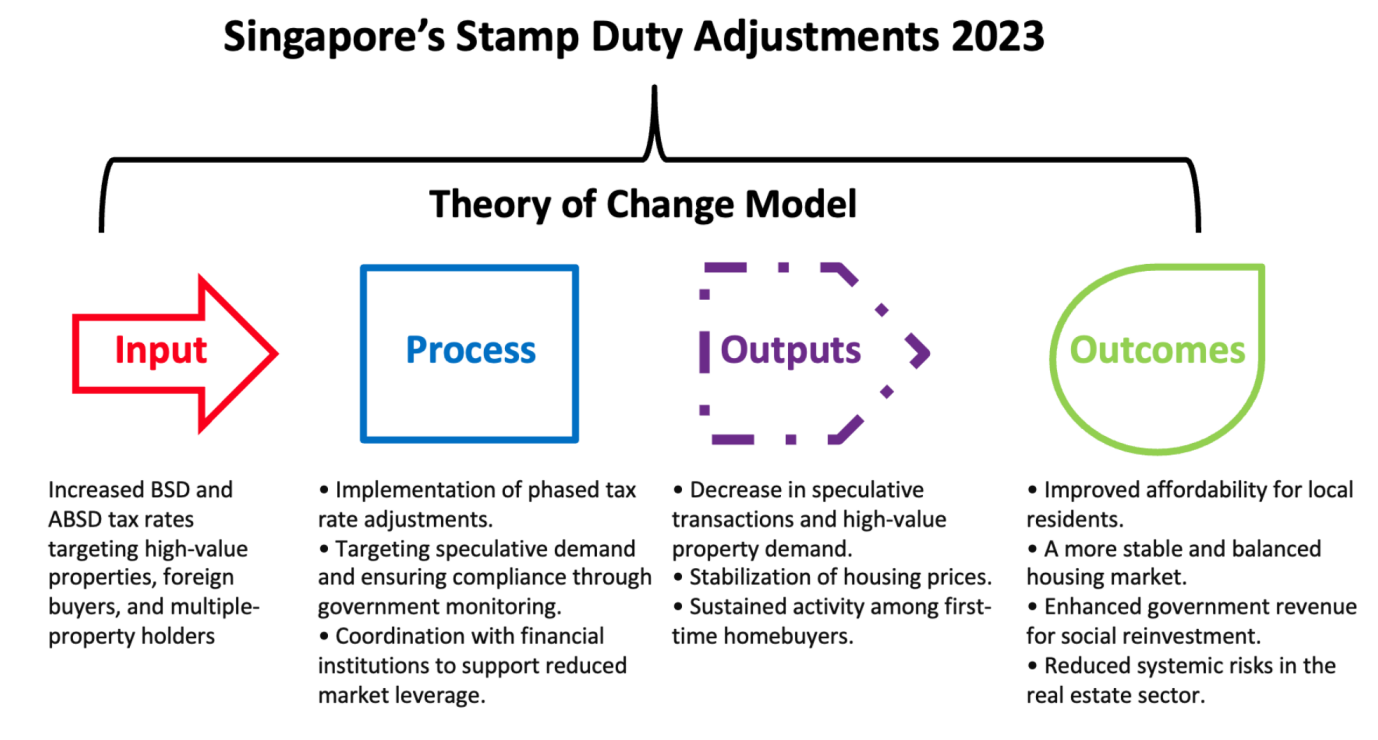

Figure 6 presents the logic and framework of the TOC model analysing Singapore’s 2023 stamp duty policy. Singapore’s policy's short-term goal is to reduce speculative demand and curb market overheating; the medium-term goal is to optimise market structure and stabilise property price growth; and the long-term goal is to achieve healthy real estate market development and promote social and economic development. The policy's target audience primarily includes foreign buyers, local multiple-property purchasers, and high-end residential buyers.

Regarding inputs, the Singapore government announced increased BSD for high-value residential properties and higher ABSD rates targeting foreign buyers and local multiple-property holders. This demonstrates the policy’s precision and differentiation, protecting the rights of first-time homebuyers while suppressing demand for high-end housing and alleviating market overheating.

In terms of process, the policy was implemented in two stages. In the first stage, BSD rates for high-value residential properties were raised. In the second stage, ABSD rates were further increased for the target audience. Government departments were responsible for policy design, announcement, and oversight during the implementation. Financial institutions and other industries indirectly supported the policy by restricting loan limits, further curbing speculative demand. For the buyer groups, the policy ensured that first-time homebuyers’ essential housing needs were protected through tiered adjustments in tax rates while significantly increasing transaction costs for high-end residential buyers, foreign buyers, and local multiple-property purchasers.

Regarding outputs, the policy is expected to have three short-term effects. First, demand for high-end housing and speculative property purchases will decline significantly. The high tax rates have doubled transaction costs, substantially reducing investor interest. Second, the growth rate of property prices will slow. The sharp decline in transactions involving high-end housing and speculative purchases directly affects property prices, as seen in Figure 3, where property prices dropped sharply in Q2 2023 before stabilising. Finally, transaction volumes in the real estate market will decrease, as Figure 4 shows a downward trend.

Regarding outcomes, the policy is expected to produce three long-term effects. First, the real estate market will remain stable over the long term. The increased transaction costs reduce speculative demand, bringing the overheated market back to rationality and lowering potential risks. Second, social equity will improve. The policy helps alleviate the issue of uneven resource allocation. As demand from speculators and foreign buyers weakens, local ordinary residents have increased opportunities to purchase homes. Essential housing needs are more easily met, improving the allocation of housing resources. Additionally, with the slower growth of property prices, it becomes easier for residents to enter the market. Finally, government revenue will grow. While the policy suppresses some transactions in high-end housing and speculative purchases, the high tax rates will generate fiscal revenue in the long run, providing financial support for Singapore’s development.

Figure 6

Using the TOC model to analyse Singapore’s Stamp Duty Adjustments 2023

Discussion

The real estate policies of Hong Kong and Singapore reflect two fundamentally different market regulation strategies: demand stimulation and demand suppression. Hong Kong’s approach to abolishing the BSD aims to reduce transaction costs, stimulate demand in the short term, increase transaction volumes, and attract returning investors to drive market recovery. However, further policy easing could risk encouraging speculative activities and driving up property prices. Enhancing market activity with speculative risks requires enhanced regulatory measures and differentiated policies (such as prioritising first-time homebuyers’ needs). Additionally, measures such as increasing land supply and lowering interest rates can provide long-term support for the policy’s effectiveness. In contrast, Singapore’s strategy of raising BSD and ABSD rates precisely targets demand for high-end residential properties and speculative activities, ensuring that housing resources are directed towards essential needs. While high tax rates effectively reduce the risk of market overheating, maintaining these rates over the long term could suppress the high-end residential market and deter capital inflows. To maintain market stability and competitiveness, Singapore will need to flexibly adjust tax rates in the future while optimising supply-side measures to increase the availability of mid to low-priced housing. These two strategies offer valuable insights for other high-demand real estate markets. They demonstrate that healthy market development can be effectively achieved through precise policy design and a balanced approach to supply and demand interventions.

Conclusion

Hong Kong and Singapore take quite the opposite ways in the Stamp Duty policy in real estate and reflect severe differences in the market environment and target of policies, governance structure, etc. MSSD and TOC also show that multiple elements, including confidence in the market, current interest rate, and comprehensive support, will play a significant role. Hong Kong’s demand-stimulation policy must be linked with a general supply side and economic incentives to generate a more significant market increase. By contrast, the demand-suppression policy in Singapore requires dynamic adjustment of tax rates to balance the market's activities with the risk of speculative behaviour. These two models are fundamental in practice for the other high-demand real estate markets and show how demand-side regulation, with a balanced approach to supply and demand, can achieve long-term market stability and social equity.

References

Anckar, C. (2008). On the Applicability of the Most Similar Systems Design and the Most Different Systems Design in Comparative Research. International Journal of Social Research Methodology, 11(5), 389–401. https://doi.org/10.1080/13645570701401552

Chen, G., Liu, X., & Yang, Y. (2023). The impact of COVID-19 pandemic on Singapore’s resilience in real estate market. Advances in Economics Management and Political Sciences, 17(1), 293–304. https://doi.org/10.54254/2754-1169/17/20231113

Cho, Y., Li, S. M., & Uren, L. (2021). Stamping out Stamp Duty: Property or Consumption Taxes? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3760893

Chui, K. H., Li, J., & Cheng, W. W. (2019). Why “spicy measures” fail to cool down Hong Kong’s housing market. International Journal of Sustainable Real Estate and Construction Economics, 1(4), 298. https://doi.org/10.1504/ijsrece.2019.10028015

Craig, R., & Hua, C. (2011). Determinants of Property Prices in Hong Kong SAR: Implications for Policy. IMF Working Paper, 11(277), 1. https://doi.org/10.5089/9781463925949.001

DATA.GOV.HK. (2024). Property Market Statistics 16. Available at https://data.gov.hk/en-data/dataset/hk-rvd-tsinfo_rvd-property-market-statistics

DATA.GOV.HK. (2024). Property Market Statistics. Available at https://data.gov.hk/en-data/dataset/hk-rvd-tsinfo_rvd-property-market-statistics

Haila, A. (2000). Real estate in global cities: Singapore and Hong Kong as property states. Urban Studies, 37(12), 2241–2256. https://doi.org/10.1080/00420980020002797

Haila, A. (2022). The Singapore and Hong Kong property markets. In Routledge eBooks (pp. 125–140). https://doi.org/10.4324/9781003280255-10

Ho, L. S., Hu, M., Wei, X., & Wong, G. W. C. (2022). The market distortion effects of mortgage tightening and transaction taxes: Evidence from Hong Kong residential resale market. Pacific Economic Review, 28(1), 142–164. https://doi.org/10.1111/1468-0106.12389

Hong Kong Special Administrative Region Government. (2024, February 28). 財政司司長財政預算案演辭(二). Government Information Service. https://www.info.gov.hk/gia/general/202402/28/P2024022800145.htm

Housing Bureau. (2024, February 28). Legislative Council reference material summary: Stamp Duty (Amendment) Bill 2024 and Public Revenue Protection (Stamp Duty) Order 2024 (LegCo Brief HDCR4/3/PH/1-10/0-1). Legislative Council of Hong Kong.

Hui, E. C. M., Zhong, J., & Yu, K. (2017). Property prices, housing policies for collateral, and resale constraints. International Journal of Strategic Property Management, 21(2), 115–128. https://doi.org/10.3846/1648715x.2016.1249984

Maye, D., Enticott, G., & Naylor, R. (2020). Theories of Change in Rural Policy Evaluation. Sociologia Ruralis, 60(1), 198–221. https://doi.org/10.1111/soru.12269

Phang, S. (2000). Hong Kong and Singapore. American Journal of Economics and Sociology, 59(5), 337–352. https://doi.org/10.1111/1536-7150.00102

Phang, S., Lee, D., Cheong, A., Phoon, K., & Wee, K. (2014). HOUSING POLICIES IN SINGAPORE: EVALUATION OF RECENT PROPOSALS AND RECOMMENDATIONS FOR REFORM. The Singapore Economic Review, 59(03), 1450025. https://doi.org/10.1142/s0217590814500258

Reinholz, D. L., & Andrews, T. C. (2020). Change theory and theory of change: What’s the difference anyway? International Journal of STEM Education, 7(1), 1–12. https://doi.org/10.1186/s40594-020-0202-3

Shao, S. W., Huang, X., Xiao, L. X., & Liu, H. (2020). EXPLORING THE IMPACT OF REAL ESTATE POLICY ON REAL ESTATE TRADING USING THE TIME SERIES ANALYSIS. The International Archives of the Photogrammetry, Remote Sensing and Spatial Information Sciences/International Archives of the Photogrammetry, Remote Sensing and Spatial Information Sciences, XLII-3/W10, 1281–1287. https://doi.org/10.5194/isprs-archives-xlii-3-w10-1281-2020

Tam, H. F. (2018). Behavioural response to time notches in transaction tax: Evidence from stamp duty in Hong Kong and Singapore WP 18/01.

ULI Asia Pacific. (2023). 2023 ULI Asia Pacific Home Attainability Index. Hong Kong: ULI Asia Pacific.

Urban Redevelopment Authority. (2023a). Private residential property market for 1st Quarter 2023. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr23-12?os=qtfTBMrU

Urban Redevelopment Authority. (2023b). Private residential property market for 2nd Quarter 2023. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr23-28

Urban Redevelopment Authority. (2023c). Private residential property market for 3rd Quarter 2023. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr23-39

Urban Redevelopment Authority. (2023d). Private residential property market for 4th Quarter 2023. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr24-03

Urban Redevelopment Authority. (2024a). Private residential property market for 1st Quarter 2024. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr24-19

Urban Redevelopment Authority. (2024b). Private residential property market for 2nd Quarter 2024. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr24-34

Urban Redevelopment Authority. (2024c). Private residential property market for 3rd Quarter 2024. Retrieved from https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr24-45

Wong, S. K., Cheung, K. S., Deng, K. K., & Chau, K. W. (2021). Policy responses to an overheated housing market: Credit tightening versus transaction taxes. Journal of Asian Economics, 75, 101330. https://doi.org/10.1016/j.asieco.2021.101330

Zhang, Y., Tu, Y., & Deng, Y. (2023). Duration‐dependent transaction tax effects on sellers and their behaviours. Real Estate Economics, 52(1), 140–183. https://doi.org/10.1111/1540-6229.12441